A Portfolio Investment Entity (PIE) is a managed fund which has a tax treatment that can provide certain tax benefits for some investors.

An individual investor in a PIE, such as the First Mortgage PIE Trust, will select a Prescribed Investor Rate (PIR). A PIR is similar to a marginal tax rate and is used to calculate and pay tax on income from a PIE. The PIE will then pay tax based on each investor’s PIR.

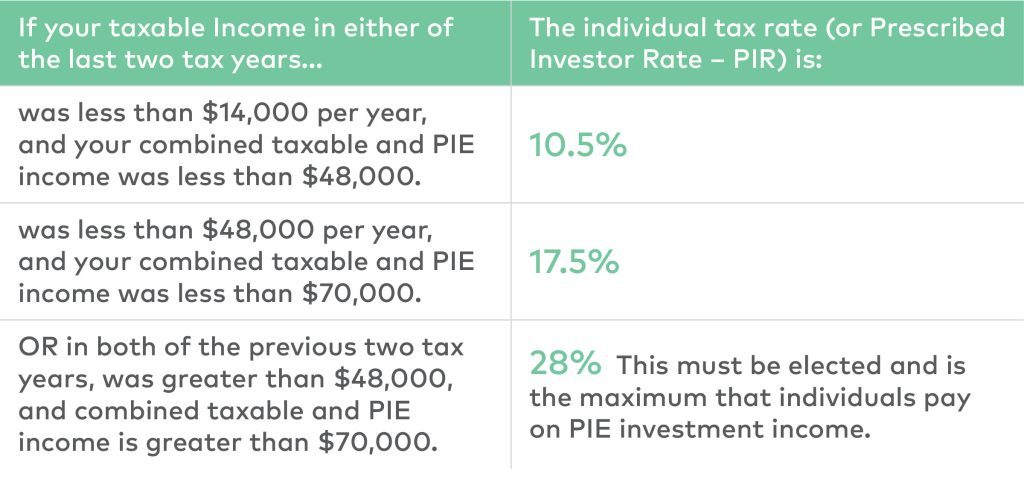

For an individual, the PIR for an investment in a PIE is determined by your previous two year’s income as follows:

Different PIRs apply to companies and other types of investors. For details, or to work out your PIR go to ird.govt.nz or speak to your tax adviser.

A PIE investment can increase the amount of income that a 10.5% or 17.5% tax rate is applied to. If an investor is able to elect a PIR rate of 10.5% or 17.5% based on the last two years income, then PIE tax paid will be a final tax in the current year even though the current year’s income may be greater than the income thresholds. i.e. PIE income may be subject to PIE tax at 10.5% or 17.5% when the same income if earned from a non PIE investment would be subject to tax at 30% or 33%.

Individuals who earned under $14,000 of taxable income (i.e. total income less PIE income) and less than $48,000 total income in either of the last two years can elect a PIR of 10.5%. Income between $14,000 and $48,000 would be subject to income tax at 17.5% if it was not received from a PIE fund.

Similarly, individuals who earned under $48,000 of taxable income (i.e. excluding PIE income) and less than $70,000 total income in either of the last two years can elect a PIR of 17.5%. Income between $48,000 and $70,000 would be subject to income tax at 30% if it was not received from a PIE fund.

Investors who have a marginal tax rate of above 28% will also benefit from 28% being the highest tax rate payable within a PIE.

Investors with First Mortgage Trust, who are in the above circumstances, may wish to transfer some or all of their existing investment – or place any new investments – with First Mortgage PIE Trust.

Disclaimer: First Mortgage Trust is not a Tax Adviser. The benefits of PIE will depend on each investor's personal circumstances. This information is of a general nature and we strongly recommend that you talk to your financial or tax adviser to determine if investing in First Mortgage PIE Trust is right for you. Tax laws are subject to change, article based on legislation in effect on date published.

It is the responsibility of the investor to tell FMT of your PIR when you invest or if your PIR changes. If you do not tell us, a default rate may be applied. If the rate applied to your PIE income is lower than your correct PIR, you will be required to pay any tax shortfall as part of year end tax assessment. If the rate applied to your PIE income is higher than your correct PIE, any excess tax will be used to reduce your income tax liability you may have for the tax year with any balance remaining refunded by Inland Revenue.

Complete this questionnaire to see what type of fund might be the most tax effective for your circumstances. Please note, this is just a guide and we recommend you seek professional tax advice.

Disclaimer – This tool is intended to provide general guidance only. This tool does not take into account your particular financial situation, objectives or goals.

There are alternative strategies which may provide better outcomes, we recommend you seek independent advice before making any investment decision. If you have completed this guide and wish to discuss this, we recommend you seek professional tax advice.